Jesse Hitt • 11 Jun 2026 • 10 min read

Jesse Hitt • 11 Jun 2026 • 10 min readState-by-State HOA Reserve Fund Requirements: A 2026 Guide to HOA and COA Reserve Fund Accounting

")

Key Takeaways

- Many states have tightened HOA and COA reserve fund laws in response to high-profile structural failures

- Mandates either address reserve studies (the plan for how much should be saved) or reserve funds (the actual savings).

- Reserve funding laws tend to be stricter for COAs than HOAs since condominiums have more shared structural elements.

- There’s no universal “good” number to have in reserves. The most prepared association boards ground their targeted reserve funding in the reality of their asset, neighborhood needs, and life cycles.

The Shifting Landscape of HOA Reserves

A lot of concern about reserve studies began in June of 2021, when a 12-story beachfront condominium in Surfside, Florida, partially collapsed in the middle of the night. Authorities later determined the Champlain Towers South event was partially caused by long-term structural degradation, which had been reported years prior, and galvanized nationwide legislative updates on HOA finances.

Prior to the collapse, condo owner associations (COA) in Florida could waive the requirement of keeping a reserve fund large enough to ensure the building’s structural integrity. That’s no longer an option for condo associations managing buildings of three stories or higher.

Florida HOA reserve laws aren’t the only ones with increasing enforcement. Along with new building inspection requirements, these state laws seek to prevent further loss of life or property from unaddressed building corrosion.

Many states have checks in place to oversee HOA reserves, mandating long-term financial stability and community preservation. These new laws pose a particular HOA reserve fund accounting challenge for older associations that have been traditionally underfunded or rely on outdated reserve studies. Compliance with your state’s reserve law is essential for maintaining good standing with the government and making your community safer for everyone.

Understanding Your State’s HOA Reserve Fund Accounting Requirements

The first step toward achieving compliance is to understand what your state requires regarding HOA reserves. Most states have different reserve fund accounting rules for COAs and HOAs, with COA requirements typically stricter.

Two different kinds of mandates

There is some important nuance between the two common types of reserve mandates. One type of mandate involves determining how much money an HOA should save, while the other involves actually saving that amount.

- A reserve study is a professional, third-party assessment of which major components (roofs, roads, pools) of the community will need replacement, when, and at what cost. It’s a long-term financial and engineering plan that generates a recommended reserve amount.

- Reserve funding is the act of setting money aside to pay for the replacements and improvements identified in the reserve study.

State requirements vary. Some mandate one of the two, some mandate both, and others mandate neither but still offer guidance in statute.

For example, Massachusetts General Law states, “All condominiums shall be required to maintain an adequate replacement reserve fund,” while the Illinois Condominium Property Act instructs that “reasonable reserves for capital expenditures and deferred maintenance for repair or replacement of the common elements” should be held.

What applies to condos (COAs)

In most states, reserve laws particularly target COAs because condos share structural components where deterioration and deferred maintenance can become life-or-death concerns. The Champlain Towers South collapse, which resulted in 98 deaths, is a worst-case example of what can happen when corrosion is not addressed.

- 13 states require a reserve study (or reserve schedule) for condos: California, Colorado, Delaware, Florida, Hawaii, Maryland, Nevada, New Jersey, Oregon, Tennessee, Utah, Virginia, and Washington.

- 12 states require boards to actually fund reserves: Connecticut, Delaware, Florida, Hawaii, Illinois, Maryland, Massachusetts, Michigan, Minnesota, Nevada, Ohio, and Oregon.

- 6 states require both a study and fund reserves for condos: Delaware, Florida, Hawaii, Maryland, Nevada, and Oregon.

What applies to HOAs

Keep in mind that most of the statutes listed above were designed for COAs specifically and do not automatically apply to your HOA. However, a few states, including California and Colorado, do have reserve laws that also extend to HOAs.

For HOAs in the other states with COA-related reserve laws, reserve obligations are typically prescribed by the association’s own governing documents, not state law. To stay in good standing, HOA boards should first check their own CC&Rs and bylaws for specifics on HOA reserve fund accounting, then consult their state statute.

State-by-State

It’s not just best practice for COA and HOA boards across the country to know the ins and outs of what their state requires regarding reserve studies and funds. In some states, for a self-managed HOA board, volunteer board members may be personally liable for failing to maintain common elements or to plan for foreseeable repairs.

- California: The Davis-Stirling Act, passed in 1985, requires HOAs and COAs to conduct visual reserve inspections every three years. Boards are also obligated to review those inspections annually and update them accordingly.

- Colorado: Colorado Common Interest Ownership Act does not mandate that HOAs conduct reserve studies, but it does require HOAs to have a written policy regarding how and how often studies will be conducted.

- Connecticut: Connecticut does require COAs and most HOAs to maintain an “adequate” reserve fund, but has no law on the books specifically requiring a professional reserve study.

- Delaware: Delaware requires COAs to maintain reserves based on a reserve study conducted at least every five years, with minimum fund requirements for properties without an existing study. There’s no statewide mandate for HOAs, but they are expected to fund reserves in accordance with their fiduciary duties and governing documents.

- Florida: COAs with shared structural components are required to conduct a Structural Integrity Reserve Study (SIRS), focusing on the current status, durability, and maintenance needs of the building’s critical structural elements. (Other types of reserve studies may also include minor and aesthetic elements in their plan.) Florida has also eliminated the option for owners to waive or reduce reserves on key structural items.

- Hawaii: COAs in the Aloha State must either have at least 50% of the replacement reserves estimated in a reserve study or, in the case of a cash flow funding plan, 100% of that estimate. The study and estimates must be based on a minimum 30-year projection, rather than the former 20-year requirement.

- Illinois: Illinois state law instructs HOAs to share a proposed budget with homeowners that includes reserves, while COAs are obligated to keep “reasonable” reserves on hand for major repairs and replacements. Neither type of association is legally required to obtain a reserve study.

- Maryland: The state mandates reserve studies for HOAs if the common-area components (roads, roofs, amenities) are valued at at least $10,000. This threshold requires boards to adopt a budget that accounts for savings for reserves.

- Massachusetts: There is no statewide mandate for HOAs or COAs to have a professional reserve study executed on a certain schedule. Massachusetts only requires COAs to maintain an “adequate” reserve fund in a separate account.

- Michigan: The Michigan Condominium Act requires associations to allocate at least 10% of their annual budget to reserve or reserve-related funding. There is no specific law mandating reserve studies, but they are recommended.

- Minnesota: COAs and HOAs must include “adequate reserve funds” in their annual budget to cover replacement of common elements the association is obligated to maintain. The statute does not mandate a professional reserve study or set a specific funding percentage, leaving the determination of “adequate” to the board.

- Nevada: Under the Common-Interest Ownership Act, most HOAs and COAs in Nevada are required to conduct a reserve study at least once every five years and maintain “adequate” reserves to cover repair and replacement of common elements. No specific funding level is mandated, but the community’s reserve savings must align with data in planning documents.

- New Jersey: New Jersey stipulates that all COAs and any HOAs with common property valued over $25,000 must conduct a reserve study every five years and have a 30-year baseline funding plan.

- Ohio: Ohio COAs must maintain enough reserve funds to repair or replace major components, and the amount set aside annually must be adequate as defined by the board. The law for HOAs is similar, except that there’s no annual percentage enforced. There are no state laws about reserve studies.

- Oregon: In Oregon, COAs and HOAs must refresh their reserve studies annually and have enough funds in reserve to cover the repair and replacement of any common property between one and 30 years old.

- Tennessee: COAs with common property valued at $10,000 or more are required to have a reserve study and update it at least every five years. No reserve funding percentages are stipulated, but boards are encouraged to use the studies to guide their financial plans.

- Utah: Utah has similar reserve study and fund laws for condominium associations and other HOAs. Boards must conduct a new reserve analysis every six years and refresh it every three. As in Tennessee, the statutes only require that boards be “prudent” in maintaining their reserve funds.

- Virginia: HOA and COA boards are obligated to conduct a reserve study every five years, review it annually, and maintain sufficient reserves to cover the repair or replacement of capital components as recommended by the study.

- Washington: Washington requires HOAs and COAs to prepare an initial reserve study based on a professional visual site inspection, with annual updates and a professional re-inspection at least every third year. The requirement doesn’t apply to nonresidential communities, those with only nominal reserve costs, or cases where the study would cost more than 10% of the annual budget.

What Is a Good Amount for an HOA to Have in Reserves?

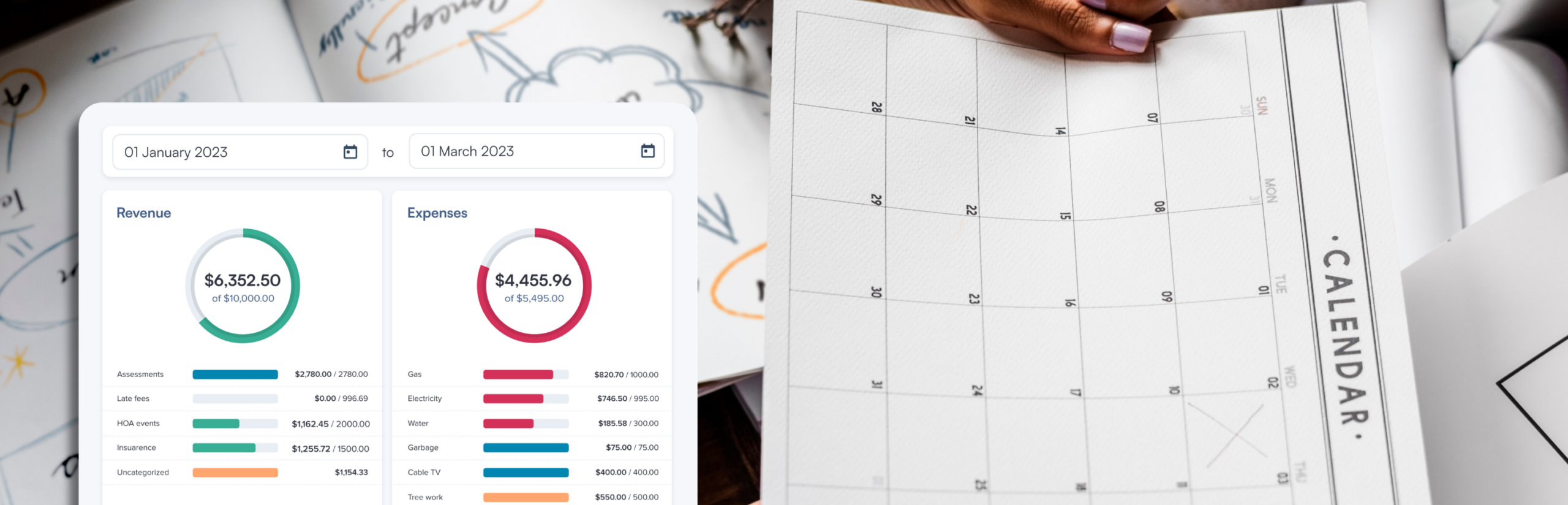

If you’re not bound to a specific reserve funding level by your state government, you’re probably left wondering what a “good” amount of money would be for your HOA to keep in its reserves. Most associations use the basic metric of “percent funded” in HOA reserve fund accounting, according to the estimate laid out in their reserve study.

In general, 0-30% funding is considered weak and carries a high risk of deferred maintenance, while 31-70% is considered fair, with moderate stability but potential gaps. Anything from 71-100% funding is considered strong, enabling associations to fulfill the replacements and upkeep required in their reserve plan without financial issues.

A statutory example of the “percent funded” metric is Hawaii’s aforementioned requirement that association reserves must be at least 50% funded at all times. However, there’s no universally “right” number for all HOAs. The appropriate funding level depends on your community’s component inventory and life cycles, which can be impacted by a number of factors, including weather. Reserve funding goals should be based on real-world projections, not random dollar amounts.

Reserve Compliance Takes Work

Even where mandates exist, the real work of reserve planning is figuring out what your community needs and funding it consistently year after year. Get it wrong, and you’re looking at underfunded repairs, special assessments, or personal liability for the board.

PayHOA brings the moving parts together. Line-item tracking for repairs and replacements, automated reserve transfers from dues, and live budget vs. actual comparisons all live in one place, so volunteer boards aren’t reconciling spreadsheets the night before a meeting. Easy to use on the surface, with rigorous reserve-planning demands underneath.For more hands-on help, PayHOA’s HOA bookkeeping service can help you build a sustainable plan before you lock in your budget. This article is informational, not legal advice. For state-specific questions, read your statute and consult a community association attorney.

Share this article:

Enjoyed this Article? Try Another!

HOA State Laws: What Every Board Needs to Know About Compliance

Key Takeaways HOA state laws are the statutes each state enacts to govern homeowners associations,…

The Guide to Colorado HOA Laws

Key Takeaways Serving on a Colorado HOA board, you likely have governing documents to follow….

How to Find a Good Lawyer for Your HOA

Key Takeaways A good HOA lawyer has proven experience in community associations in your state,…